Author Archives: ACA Reporting Service

03

Dec

Dec

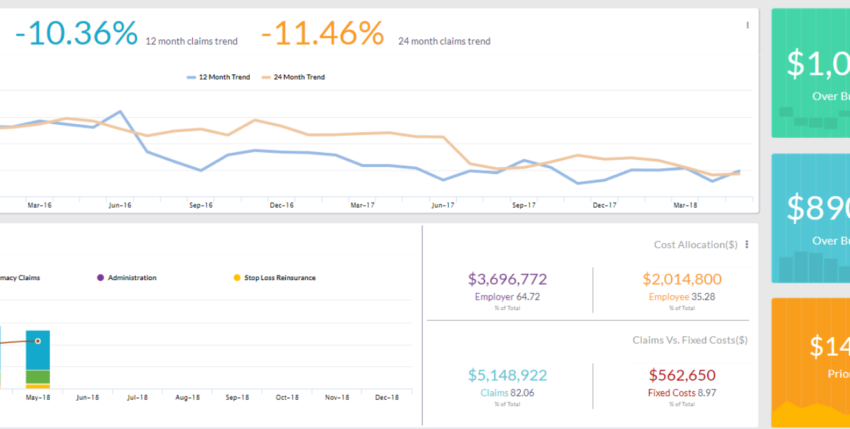

We are pleased to announce a strategic partnership with Self Insured Reporting to the benefit of our clients.

SelfInsuredReporting.com is a financial reporting and claim analytics system specifically designed for self insured employers. Their platform helps you quickly answer questions such as:

- How is our plan performing versus our budget for the year? How about our stop loss contract?

- What are the costs expected to be for the rest of the plan year? What is my expected renewal?

- How are the medical and pharmacy claims trending for each plan? What about network performance?

- How are claims trending for conditions such as cancer or diabetes?

- Which providers are the most expensive in an area?

- Are there opportunities to ‘drive’ services from one provider to a lower cost provider, such as from an emergency room to an urgent care facility?

Learn more at SelfInsuredReporting.com

22

Oct

Oct

By now, many employers have received penalty assessments (Letter 226J) for noncompliance with the employer mandate in the tax year 2015. These penalty letters where not issues until Nov 1st of 2017. However, U.S. Treasury Inspector General for Tax Administration (TIGTA) reports from this year show that the IRS is gearing up to begin issuing penalty letters for the 2016 tax year very soon.

At Sky Insurance Tech, we do a good deal of penalty consulting for prospective clients. These are almost always clients that did their reporting with a lower priced, sub-par vendor, if they did their reporting at all. Recently, we have been getting a ton of phone calls regarding letter 5699 from the IRS for the 2016 tax year.

Letter 5699 is what the IRS uses to inquire about an employer’s reason for not properly filing their forms 1094/1095C. Employers who receive this letter have 30 days to respond. If the employer cannot prove that the letter was sent in error, then there is serious consequence, including a letter 226J for the 2016 tax year.

The IRS didn’t issue 2015 letter 226J penalty assessments until November 1st of 2017. However, November 1st of 2018 is right around the corner, which is the time frame we are expecting to see the 2016 penalty letters released. It is also important to note that just because the 2016 notices are set to be issued, this does not mean that the 2015 notices are finished being distributed.

For these reasons we encourage employers to revisit their previous year’s filings. Make sure that these were both accurate and timely.

If assistance is needed with either previous reporting years, or with penalty notices from the IRS, we are here to help.

29

Jun

Jun

On Wednesday June 27th the New Jersey Health Insurance Market Preservation Act was signed into law. This was just the latest development in an effort for several states who are attempting to enact Mandated health insurance at the State level.

The New Jersey law in effect enforces residents, by way of penalty, to enroll in qualified health insurance. This law will be enacted on October 1, 2018 and will apply to taxable years beginning Jan 1, 2019.

It is being said that in many ways this Mandate was designed to mirror the Mandates brought forth by the Affordable Care Act (ACA). Here are a few of the similarities:

- Annual penalty of 2.5 percent of a household’s income or a per-person charge

- Maximum penalty based on household income will be the average yearly premium of a bronze plan in the state (rather than nation like the federal law)

- maximum penalty based on per-person charge will be a maximum household penalty of $2,085

Reporting Guidelines

Along with this come reporting requirements. Employers will have to report qualified offers of coverage to individuals to track subsidy eligibility. The bill states that “In summary, any reporting that was acceptable under the ACA’s federal guidelines will be accepted under the New Jersey’s state reporting guidelines”.

Other States to Potentially Enact Health Insurance Mandates

Massachusetts was the first state to enact a health insurance mandate (took effect in 2006 and was a model for the health insurance mandate in the ACA). It is still implementing this mandate.

Vermont governor, Phil Scott, signed a bill on May 28 that would establish an individual mandate. The details for the bill such as financial penalties and enforcement mechanisms will not be determined until the 2019 legislative session, which means the mandate won’t go into effect until January 1, 2020.

Maryland Democrats running for Governor have all agreed to a health insurance program that has many ACA related items. The insurance program will create a state individual mandate where the penalties imposed on individuals for not obtaining health coverage would be used as a “down payment” to obtain health insurance policies.

Other states that have discussed the possibility of a state individual mandate are; California, Connecticut, Hawaii, Minnesota, Rhode Island, Washington, and District of Columbia. Many of these states’ ability to implement an individual mandate will hinge on the results of the midterm elections this November and how many Democrats are voted into office.

It has been rumored that if these states are able to enact Healthcare Mandates they will do so with the intention of having their state laws closely mirror the infrastructure of the Affordable Care Act. Several of the states are attempting to use re-insurance coverage to take care of the expense associated with higher risk individuals. It has been reported that penalties associated with the Mandates and subsequent reporting will be used to fund these re-insurance premiums.

Overall Outlook

A few weeks ago, we published an article outlining the potential impact of the upcoming Mid-Terms as it pertains to Health Care reporting. That Article can be found here.

It seems that the Mid-Terms will take a determining role in how this all plays out. However, these laws being taken to the State level are a sign that no matter the outcome on the Federal level, there are many states who are ready to enact “ACA like” laws of their own.

The IRS is currently enforcing the Individual Mandate at the Federal level for 2018. Additionally, enforcement of the Employer Mandate continues to occur. Letter 226J is being sent out for the tax year 2015, and our sources are saying that 226J letters for 2016 are soon to follow.

Right now, may be a very good time to retroactively review your previous years filings

Uncategorized

How will the upcoming mid-terms affect the need for Employer based healthcare reporting?

12

Jun

Jun

A LITTLE BIT OF CONTEXT

Here we are, 2018 and staring down the barrel of another upcoming election. This time will it be the Democrats who takeover control of congress? Will the Republicans maintain their stronghold and gain seats? How will the outcome of this election shape the landscape for ACA reporting going forward? The answer might not be what you think.

We’ve watched for years now as Republicans have fought to fulfill their promise of dismantling the Affordable Care act and along with it, the unpopular Employer Mandate. This mandate has required employers with 50 or more full time employees to offer certain healthcare coverage then report their offers of coverage via informational returns (1094/1095Cs) that are then supplied to employees. These reports are ultimately filed with the IRS. Failure to comply with this law can result in millions of dollars’ worth of penalties for the employer. So how can the 2018 midterm affect this?

The broad consensus that we are hearing at Sky Insurance Tech is that if Republicans gain seats and Democrats lose seats, the Employer Mandate will go away and so will the need to report coverage.

To that notion we say, “HOLD YOUR HORSES”.

This common misconception comes from the assumption that ACA Reporting is tied directly to the Employer Mandate. If the Employer Mandate goes away, so does the need to report. That would be a risky assumption. So, I will do my best to explain in the paragraphs that follow, why that thought process is totally incorrect.

THE REPORTING IS ALL ABOUT THE SUBSIDY ELIGIBILITY

First things first, what are we talking about with ACA Reporting? Why do employers have to report their offers of coverage? To be compliant with the ACA laws of course! Right, however lets really think about why this is part of the law. This is part of the law because of Subsidized health coverage.

That’s right, the reason reporting exists is because healthcare subsidies exist, and we must determine who is eligible for a subsidy and who is not. An Employers offer of affordable coverage greatly affects an individual’s subsidy eligibility. Universally granting subsidies would be catastrophic for the US budget, so we must determine who needs this assistance.

So, there’s your short answer. No matter what happens to the ACA law, if there are subsidies there will be reporting.

Here is where the rebuttal comes in, “well what if we get rid of the subsidies altogether”? Really? Do you think that is a possibility at this point? I think now is a good time to take a closer look at the numbers, then we can formulate a more educated opinion.

ALL ABOUT THE SUBSIDIES

Based on a recent report released by the Congressional Budget Office (CBO), in an average month in 2018, about 244 million people under the age of 65 will have health insurance, and around 29 million people will not. By the year 2028 it is projected that the 29 million number will grow to around 35 million. Currently net federal subsidies for “Insured” people in 2018 total around $685 Billion. These subsidies are expected to grow to 1.2 Trillion in the year 2028. These subsidies are being used to help pay for: Medicaid, The Children’s Health Insurance Program, Medicare, and coverage obtained through the ACA Marketplace. So, at this point we must ask these questions: Can we really get rid of these subsidies? If we attempt such a thing what would be the outcome? How would this affect the American people?

WHAT DO SUBSIDIES LOOK LIKE GOING FORWARD?

According to the CBO, an average month in the year 2018 will look about like this.

- 158 million people will be enrolled in Employment based coverage.

- 12 million people will be eligible for Medicaid due to the expansion brought about by the ACA.

- 49 million will be eligible for Medicaid.

- 6 Million people in the Children’s Health Insurance Program.

- 8 million people on subsidized healthcare coverage from the ACA marketplace.

- 2 million people on unsubsidized coverage from the marketplace.

- 8 million on Medicare.

- 10 million on other coverage.

- 29 million uninsured.

Additionally, health insurance premiums are expected to increase by about 15 percent on average between 2018 and 2019. Then they are expected to increase at a rate of around 7 percent a year between 2019 and 2028.

So where will the money come from to cover all this healthcare? Subsidies of course! I think now is a good time to mention something else. Even If the law changes, and we replace the word “subsidy” for let’s say……. the word “tax credit”, we will still be in the exact same situation.

We will have a growing demand for healthcare coverage, and a growing number of people of who cannot afford it. The strain on the US budget is enormous and growing and we must consistently track subsidy eligibly or else risk massive overspending.

There is simply no way to keep up with subsidy eligibility outside of Employer Based Reporting.

HOW DO WE MITIGATE THE COST OF SUBSIDIZED HEALTHCARE?

There is a short answer to this question as well, taxes and penalties.

These taxes and penalties are expected to reduce the total amount of federal subsidies for coverage by about $21 billion in 2018. Most of these will come from penalties associated with the employer mandate. The IRS is currently enacting those penalties and notifying employers through the issuance of letter 226-J.

HOW WOULD REPORTING BE ENFORCED?

In this article we’ve been talking about a scenario in which the Employer Mandate goes away. (A broad assumption that assumes a Republican Majority and the ability to garner the needed votes). So, in this scenario how would any of the reporting be enforced.

The reporting itself has been and will continue to be enforced by the US Code § 6721 and § 6722. Those are as follows:

26 U.S. Code § 6721 – Failure to file correct information returns

26 U.S. Code § 6722 – Failure to furnish correct payee statements

What these laws state, is that there are penalties associated with not filing correct and timely informational returns to the IRS. Additionally, there are further penalties associated with not furnishing those same returns to employees on time.

The existence of these laws does not hinge on the Employer Mandate remaining the law of the land. However, they will exist if subsidies and/or tax credits exist. These will remain enforceable as long as subsidy eligibility is something that needs to be tracked, and due to costs, they must be tracked.

IN CONCLUSION

At this point hopefully, you now understand why it would be incredibly difficult to remove the need for Large Employers to report their offers of health coverage. Additionally, I hope I’ve done a decent job of explaining the struggle surrounding the notion of removing billions of dollars of healthcare coverage for millions of Americans.

Can we totally remove healthcare subsidies? I don’t think we can, but you are free to decide.

Can the US afford to not regulate subsidy eligibility? I don’t think we can do this either.

Would we need to know details of the offers of coverage from employers for Subsidy eligibility? Yes.

Would that require a form of Employer Reporting similar to what we have now? Absolutely

Unfortunately, there is no crystal ball telling us about the future. Only time will tell us the outcome for certain. Based on the evidence thus far I revisit the question. How will the upcoming mid-terms affect the need for Employer based healthcare reporting? My answer, it won’t.

The IRS maintains a very comprehensive Frequently Asked Questions (FAQ) document regarding ACA compliance for employers and until yesterday they had been silent regarding the enforcement of employer mandate penalties. That now has changed, and employers should expect to begin seeing penalty letters in November and December of 2017. These first letters will be for the enforcement of 2015 ACA penalties and will begin their efforts to audit compliance.

So with this update we now know a few things:

- Is the IRS going to enforce the ACA employer mandate penalties?

- Yes, beginning with the 2015 reporting submitted by employers.

- When will they begin enforcing for the 2016 calendar year reporting for ACA?

- We expect this to begin in the early part of 2018.

- How will employers be notified?

- This will be done through a letter called “Letter 226J” which will include all of the details about what penalties you will be responsible for paying. You can learn all about ACA penalties from this link on our website.

- What will be included in the IRS letter?

- These letters will also include a Form 14765 which will outline in detail the month that employees received tax credits for reduced health premiums from the exchange and will therefore mean the employer will own a shared responsibility payment/penalty.

We are still helping employer with their 2015 and 2016 prior year reporting, and still accepting clients for 2017. So please let us know if we can be of assistance. Also you can visit the IRS updated FAQ and see all of the details from this link.

Today the IRS has issued a warning that they will begin implementing the ACA mandate penalties. Also, they will not accept 2017 income tax returns that do not comply with the Affordable Care Act rules which require each person to disclose the type of health insurance coverage they maintained for the year.

“Obviously, this has an impact on employers. Most employers have worked to stay compliant with the requires ACA reporting requirements, however there still are many employers … believe it or not … who have simply disregarded reporting up to this point. With the mandates being enforced, this is going to be expensive for those who have disregarded their reporting.”

To view the IRS notification to tax professionals, click here.