In the Beginning….

Last November the world watched as Republicans won the white house along with majority control of Congress. With the notion of “repeal and replace” being at the forefront of almost every Republican campaign, it seemed as if quick action toward that end was inevitable. House Speaker Paul Ryan along with Senate Majority leader Mitch McConnell (R-Ky) almost immediately began moving forward with what they were calling a “Straight Obamacare Repeal Bill”.

The aim of the bill would be simple. Repeal the Affordable Care Act (Obamacare) now, then allow for a two-year transitional period to craft a replacement. The plan seemed to be gaining momentum until Trump did an interview with CBS’s “60 Minutes”. In that interview, Trump notoriously stated that he planned on repealing and replacing the healthcare law simultaneously.

Shortly after, Paul Ryan began working with Trump to help craft a bill that would simultaneously repeal Obamacare and then provide a replacement program. What ensued were nine months of uncertainty, several failed votes and ultimately the death of Obamacare repeal attempts.

What Came Next Was Time Consuming

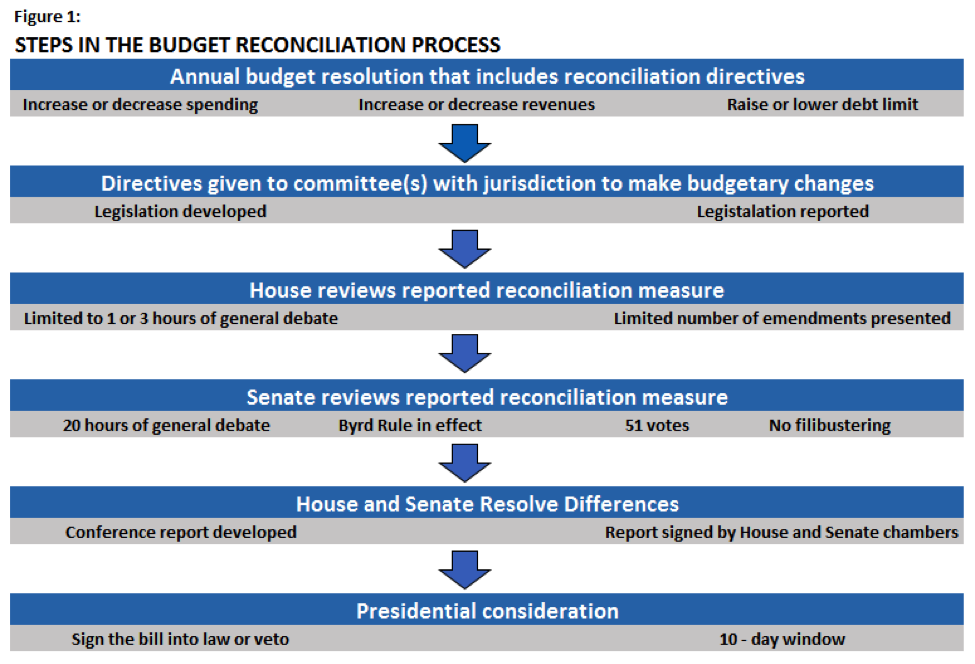

To avoid a Senate filibuster which would require 60 Senate votes to overcome, congress elected to use what is known as “Budget Reconciliation” in their attempts to dismantle the healthcare law. This procedure only requires a simple 51 vote majority and cannot be filibustered. Since Senate republicans held 52 seats, they could afford to lose up to two member votes on any proposed bill and still have it pass with vice president Pence available to break a tie. It all seemed inevitable given the majority numbers.

However, disagreements began to arise in Congress with regard to the repeal efforts very shortly after Trumps inauguration. House moderates debated many aspects of repeal with house conservatives and vice versa. What ensued were delays, then even more delays.

Republican momentum began to fade as February came and went. It became evident that Republicans did not have a repeal bill crafted prior to the election. It was March before a bill was finally marked up by the Committee on Ways and Means.

A House vote was scheduled for March 24th. Trump told Republican law makers “it was now or never”. On the day of the scheduled vote it became evident that Ryan did not have the votes. Ryan drove to the white house to personally inform Donald Trump that they had failed. Afterwards Ryan stated that Obamacare would be the law of the land for the foreseeable future. Trump was furious in defeat and congress left for a two-week Easter break.

The First Resurrection

Just weeks after the failed House attempt, the chairman of the conservative House Freedom Caucus declared that he was working with the moderate Tuesday Group to work out a deal.

In late April House Republicans seemed to agree on changes to the proposed bill and planned a vote for May 4th. The house passed their version of the Obamacare Repeal and Replace bill on May 4th. What ensued was a victory celebration for Trump and fellow Republicans in the White House Rose Garden. Nonetheless, the bill had only just passed the first chamber of Congress and still had some ways to go.

The Fight in the Senate

The victory in the House was followed by some bad news shortly thereafter. It seemed that many of the changes that helped win over House Conservatives, really didn’t sit well with Senate Moderates.

The first to speak up was Senator Susan Collins (R-Maine) who declared that the Senate would be “starting from scratch”. This meant they were practically throwing out the House version of the bill, and whatever the Senate would draft would then need to be reconciled again with the House. A tall order indeed.

McConnell decided to set up a working group to have hearings and conduct an open process for the American people. Notably, not a single female was assigned to the working group. This oversight became important because proposals to defund Planned Parenthood and allow states to obtain waivers with regard to maternity care, proved to be very unpopular with women. This resulted in controversy and delay.

A Senate Bill Emerges

The Senates legislation titled “the Better Care Reconciliation Act” was released on June 22nd. Many of the bills details had been kept secret and several Senators felt “out of the loop”. Days before the release of the bill, many members of Congress were still clueless as to what the bill contained.

A vote on the bill was postponed after four Senate conservatives – Sen Ted Cruz (R-Texas), Sen Rand Paul (R-Ky), Sen Mike Lee (R-Utah), and Sen Ron Johnson (R-Wis) – all criticized the bill for not dismantling the ACA enough. What followed was a mad dash by Mitch McConnell to win over skeptical conservative and moderates alike. Several amendments were made and finally the bill seemed to be at a place in which it was ready for a vote.

Can’t do it Without McCain

In July Sen John McCain (R-AZ) underwent emergency surgery to treat a brain tumor. His absence took away a key Republican senate vote. The Senate would need to wait on him to recover and return to Capitol Hill before moving forward.

In waiting for McCain’s return, Republican Senators Collins (R-Maine) and Murkowski (R-Alaska) had already publicized their opposition to the Senate bill. This left the Republicans with zero margin for error. At this point they could not afford one more Republican defection if they planned on passing a bill under reconciliation. The defections of Collins and Murkowski angered President Trump who lashed out against them over social media. In hindsight, many would say this move backfired as it only angered Murkowski giving her fuel to remain an opponent of the bill.

The proposed Better Care Reconciliation Act lost traction and it was clear that the Senate did not have the votes it needed to pass the Repeal and Replace bill. Insert plan B, make a push to vote on what was deemed the “Skinny Bill”.

The Skinny Bill was nothing more than an attempt the repeal the mandates and defund Planned Parenthood. Many in the Senate did not like the idea, but McConnell thought it was a good way to start negotiations with the House. Concerns mounted as many worried the House would just simply pass the bill “as is” to show they “accomplished” something with regard to repeal.

After days of debate, McConnell surmised he had the Senate votes and brought the bill to the floor. It was well after Mid-Night on July 27th when the voting took place. Everything seemed to be going well for the Republicans until Senator John McCain notoriously gave a thumb down to the bill on the Senate floor, thus destroying the last attempt at repeal. Shortly after, McConnell conceded defeat on the Senate floor.

It seemed as if Republicans were finally coming to terms with defeat and were ready to give up on their Repeal efforts, or so we thought.

Another Resurrection?

In September Sen Lindsey Graham (R-SC) and Sen Bill Cassidy (R-La) began gathering support for their version of a repeal bill aimed at dismantling Obamacare’s subsidy programs and Medicaid expansion.

The idea was to simply provide block grants to the states, repeal the mandates, get rid of the exchange, stop Medicaid Expansion and then let the states decide what to do.

Republicans were looking at a firm Sept 30th deadline to do all of this, as this would be the end point for their Budget Reconciliation. Week after week the bill seemed to gain steam as more and more supporters gathered around the effort.

Senator Rand Paul was among the first to come out against the bill stating that it did not do enough to repeal the ACA. Shortly after, McCain and Collins both publicly announced their opposition to the bill. On Tuesday September 26th Graham and Cassidy admitted defeat as yet another attempt at repeal fell into failure.

Moving Forward

On Friday Sep 29th, a draft of the Congress budget resolution was released. This draft did not include any specific instructions with regard to health care reform. It can be assumed this means that efforts to repeal the Affordable Care Act must now wait until 2019. However, that supposes that Congress maintains GOP majority through the 2018 mid-term elections. The Senate may be ok, but the house may be at risk.

Currently Democrats are leveraging the Obamacare repeal failures against the Republicans building up to the 2018 mid-terms. It is widely thought that future attempts to repeal the law will be wildly unpopular and difficult for the Republicans in Congress.

What this means is that The Affordable Care Act (Obamacare) remains the law of the land. It means that the Employer Mandate is staying in place, and it also means that we should expect the IRS to implement any and all penalties that pertain to ACA compliance and Reporting. For the foreseeable future, none of that is going to change.